Over the last 3 years I’ve been devising a method to facilitate investing at the local level in ways that are simple, legal, and beneficial to all involved (investors, the businesses receiving the investment, and the communities in which they reside). This endeavor poses significant challenges and it’s success is by no means assured. However, the thought of looking back and wondering what might have been compelled me to make a difficult decision.

In order to accomplish this, I had to resign as a financial advisor.

I’ve come as far as I can with planning, now it’s time for action. Time to take a risk and see if I can create change where I see a need.

Until I’m ready to officially launch, I’ll be helping the local economy through my efforts at Workshed, where I’m able to directly apply my skills, knowledge, and experience to help businesses connect with customers.

Stay tuned, it should be an interesting experience.

Columbia Property Trust Announces IPO Date and Tender Offer

On September 30, 2013 Columbia Property Trust released a statement with 2 important details about the upcoming IPO. The first is the listing date, on or about October 10, 2013 under the symbol CXP. If all goes according to their plan, Columbia Property Trust will be a publicly traded company in less than 2 weeks.

In conjunction with the IPO they also announced a tender offer to buy back up to $300 million of it’s common shares in a “Dutch Auction.” Details about the tender offer price have yet to be released, but I’ll post them as soon as I read through the regulatory filings.

UPDATES: October 10, 2013

Columbia Property Trust released the details of the dutch auction. The price range will be from $22.00 to $25.00 and will be available for 20 days after the IPO.

I started a page to make organizing the information easier, view it here:

On September 20, 2013 Columbia Property Trust announced in their latest Quarterly Update, plans for a public offering on the New York Stock Exchange in October, a dividend cut from $0.38 to $0.30 per share, and the addition of 2 Independent Directors to their Board.

I’ve created a special page for up to date information on Columbia Property Trust here:

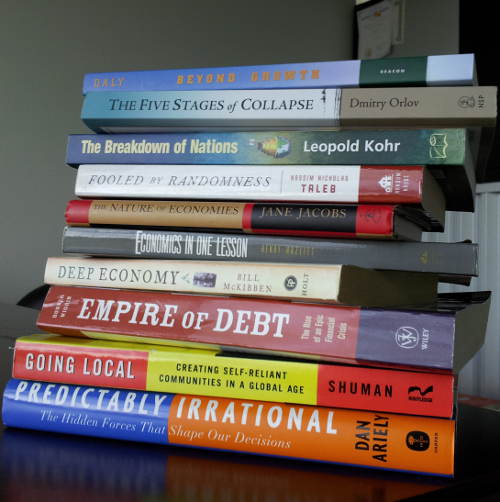

Being an elected representative carries a tremendous responsibility. Decisions made while in office impact their current constituents, but more importantly – they linger long after they have left office.

Because of this legacy effect, and the reality of unintended consequences, it is and should be, imperative that public servants learn all that they can about the critical issues facing those they are elected to represent. Sadly, the commentary and actions from the local, state, and national politicians tells me this is not happening. As such, I’ve prepared a short list of books that should be read as a primer for those entering public service, as well as those already serving.

While I’m at it, I may as well include everyone that is represented by elected officials too. It’s difficult to engage in meaningful debate when most citizens understanding of their civic duty is limited to sound bites from television and radio personalities.

On August 15, 2013 Columbia Property Trust (Formerly Wells REIT 2) sent a letter to investors outlining their plan for a reverse stock split and introducing a new CFO. Here’s my summary of what’s they have to say.

Bank loan or floating rates bonds are unique among bond types in that the rate is not fixed, but is free to move in relation to an underlying base rate such as the LIBOR (London Interbank Offered Rate). As with any investment there are risks and bank loans are no exception. With the prospect of rising interest rates looming over our economy, everything from bonds to houses will be impacted so I’m constantly looking for ways to benefit from that environment.

Virtus Investment Partners published a white paper in May of this year discussing floating rate funds and their characteristics.

Author and speaker James Howard Kunstler is perhaps the most outspoken critic of suburban sprawl and alternative energy as a replacement for cheap oil. In a pair of TED talks in 2004 and 2010 he shares his perspective and explains how our we lost our “places.” (a word of caution: Kunstler uses colorful language at times)

For a deeper dive into how we got to where we are and some thoughts on where we might be going Kunstler also wrote a few books worth reading:

Luis von Ahnm created Captcha to suppress spam on the internet and launched reCaptcha when he realized the potential of massive online collaboration to help digitize books. Now he’s doing the same for language learning and translation with DuoLingo.

I’m relearning spanish right now, if you want to join me check out my profile here: Joe’s DuoLingo Profile